BMW driver demographics statistics at a glance

BMW drivers are not a single buyer type.

The dataset points to a highly segmented audience shaped by age, gender, income, household composition, and attitudes toward electrification.

Key takeaways:

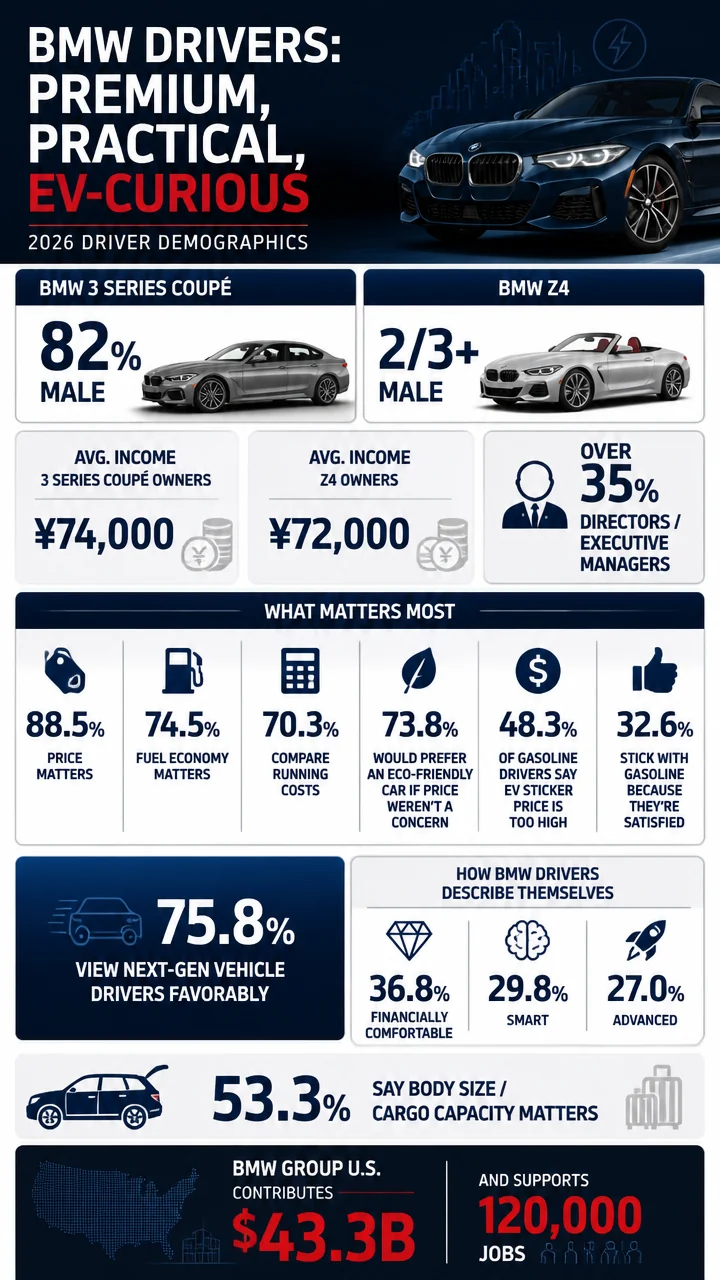

- BMW ownership skews male in several model-specific datasets, including 82% male for the BMW 3 Series Coupé and more than two-thirds male for the BMW Z4.

- Premium BMW owners often have high incomes, with the BMW Z4 owner average at ¥72,000 and the BMW 3 Series Coupé owner average at ¥74,000.

- EV and next-generation vehicle interest is strong, but cost remains the main barrier across Japan, the U.S., and Canada.

- BMW customers and prospects consistently value innovation, operating costs, and range over hype alone.

Big number: BMW Group in the U.S. contributes more than $43.3 billion to the economy annually and supports over 120,000 jobs.

BMW driver demographics statistics: the core ownership profile

The strongest pattern in the data is clear: BMW drivers are often described through a premium, professional, and business-oriented lens, especially in model-specific surveys.

That profile shows up again and again in the age, gender, household, and income figures.

Fast fact: BMW 3 Series Coupé owners were 82% male, while over 35% were directors or executive managers.

The model data suggests BMW is especially strong among people who see cars as part of a professional identity, not just transportation.

The clearest examples come from the 3 Series Coupé and M5, which both skew toward high-usage, higher-income, business-aligned owners.

- BMW 3 Series Coupé owners were mostly men and heavily concentrated in senior business roles.

- BMW M5 owners were typically male, married, and above average income.

- BMW Z4 owners were also predominantly male, with the biggest age group in the 30-39 bracket.

BMW driver demographics by age, gender, and income

BMW’s model-level buyer data shows how sharply ownership can differ by vehicle type.

Some BMW models lean toward younger professionals; others are more business-centric or lifestyle-oriented.

| BMW model | Age profile | Gender split | Income / occupation snapshot |

|---|---|---|---|

| BMW Z4 | Biggest age group: 30-39 | More than two-thirds male | Average annual household income: ¥72,000 |

| BMW 3 Series Coupé | 29% aged 30-39; 28% aged 40-49; 29% aged 50-59 | 82% male | 75% senior business people; average income ¥74,000 |

| BMW M5 | Typical owner: 45 years old | Average customer: male | Above-average income; found in all self-supporting professions |

Why it matters: BMW’s demographic appeal is not just “premium.” It is premium in a very specific way: affluent, professionally active, and often mid-career or established buyers.

One of the most interesting details is how the 3 Series Coupé spreads across a broad middle-age range.

With 29% aged 30-39, 28% aged 40-49, and 29% aged 50-59, the buyer base is unusually balanced across three adjacent life stages.

BMW ownership and household structure

Household vehicle counts also reinforce BMW’s premium positioning.

Many BMW owners are not choosing a car as their only vehicle.

- Most BMW 3 Series Coupé owners had two cars in the household.

- 11% had three cars in the household.

- BMW M5 owners also averaged two further cars in the household.

This pattern suggests that BMW ownership often sits inside a multi-car lifestyle, especially among higher-income households and business users.

BMW driver demographics statistics and EV attitudes

Across Japan, Canada, and the U.S., the data shows a clear tension: people are interested in cleaner and more advanced vehicles, but price and practicality still dominate the decision process.

Standout figure: In Japan, 88.5% of drivers said price is a factor when choosing a car, making cost the single most important consideration in the survey.

That price sensitivity is echoed in almost every dataset here.

Even when people want next-generation or electric vehicles, many still hesitate because of sticker shock, operating uncertainty, or a preference for hybrid bridges before full battery-electric adoption.

BMW driver demographics statistics: Japan survey trends

The BMW Japan next-generation vehicle survey is packed with signals about what drivers value and where adoption stalls.

The biggest message is that consumers like the idea of newer technology, but economics remain decisive.

| Japan survey metric | Share of respondents | What it suggests |

|---|---|---|

| Price is a purchase factor | 88.5% | Cost is the top filter in vehicle choice |

| Fuel economy matters | 74.5% | Running costs remain central |

| Prefer environmentally friendly car if price were not a concern | 73.8% | Desire exists, but affordability limits action |

| Carefully compare running costs | 70.3% | Consumers are actively cost-aware |

| Body type, size, or cargo capacity matters | 53.3% | Practicality still matters more than image alone |

| Want a next-generation or hybrid car in the future | 58.3% | Interest in transition technology is broad |

Pull quote: 73.8% of Japanese drivers said they would prefer an environmentally friendly car if price were not a concern.

That single figure is especially revealing.

It shows demand exists, but affordability is the bottleneck.

The same theme appears in the gasoline-car driver subgroup:

- 48.3% said they do not buy next-generation cars because the sticker price is too high.

- 32.6% said they are satisfied with gasoline cars.

- 55.0% of respondents who were not attracted to next-generation cars cited high vehicle price as the reason.

- 49.6% of gasoline-car drivers said they want to switch to a next-generation or hybrid car.

That last number is particularly important.

Nearly half of gasoline-car drivers are open to switching, which means the market barrier is not rejection of the idea — it is the economics of the purchase.

Japan survey: younger drivers and knowledge gaps

Age matters too.

Younger respondents appear less engaged with ownership economics than older drivers.

Notable split: 42.5% of people in their 20s said they do not much consider running costs or have never thought about them.

That helps explain why messaging about savings, maintenance, and charging or fuel costs can be more effective than broad environmental language alone.

It also suggests an opportunity for BMW-style premium brands to explain value in practical terms.

Knowledge about emissions is another gap:

- 25.5% correctly identified NOx as a vehicle air pollutant.

- 22.8% correctly identified PM as a vehicle air pollutant.

These low recognition rates show that technical environmental literacy is still limited, even in a survey that strongly favors cleaner vehicles in principle.

BMW driver demographics statistics: Canada electrification insights

Canadian respondents show a similar mix of concern and curiosity.

They are worried about the cost of running conventional vehicles, and a significant minority are actively thinking about EVs.

Fast fact: 79% of Canadian drivers were concerned about the operating costs of internal-combustion vehicles.

- 25% were considering buying an electric vehicle within two years.

- 66% of men said they were the primary decision maker when buying a new vehicle.

- 47% of women said they were the primary decision maker.

- 75% of men said they were knowledgeable about EV technology.

- 50% of women said they were knowledgeable about EV technology.

- 79% of Canadian women said helping the environment is important when considering an EV.

- 65% of Canadian men said the same.

The Canada data highlights a familiar pattern: men report higher ownership confidence and higher EV knowledge, while women place even more emphasis on environmental benefits.

Why it matters: BMW’s electrification messaging may need to balance technical confidence, environmental value, and cost realism to resonate across gender segments.

BMW driver demographics statistics: U.S. EV openness, range, and adoption signals

The U.S. datasets are especially useful because they show both attitude and behavior signals.

Americans are open to EVs, but not necessarily ready to jump straight into full battery-electric ownership.

Big number: 92% of Americans said continued innovation in EV technology is important.

That is a powerful headline for any BMW brand or product story.

Innovation is clearly a priority, and it aligns neatly with BMW’s premium-tech brand identity.

| U.S. EV survey metric | Share of respondents | Interpretation |

|---|---|---|

| Innovation in EV technology is important | 92% | Innovation is nearly universal as a value |

| Open to hydrogen fuel-cell vehicles | 58% | Alternative powertrains have meaningful curiosity |

| Consider EV buyers early adopters | 62% | EV ownership still carries an early-adopter image |

| Future EV buyers cite cost as the main barrier | 40% | Affordability remains the biggest obstacle |

| Would consider a hybrid or plug-in hybrid first | 66% | Many buyers want a transition step |

| 75 miles of daily range is sufficient | 75% | Range expectations are more modest than often assumed |

| Know nearest public charging station | 47% | Convenience knowledge is improving |

Several of these findings work together.

The fact that 66% would consider a hybrid or plug-in hybrid before a battery-electric vehicle suggests a practical, phased approach to electrification.

Likewise, 75% saying 75 miles of daily range is sufficient indicates that many drivers need less daily range than marketing narratives often imply.

Stat highlight: Nearly 20% of Americans plan to buy an EV in the next 3-5 years, and 55% expect to purchase an EV in the future.

That combination matters for BMW because it reveals a broad long-term opportunity even when immediate conversion is incomplete.

The market is not “EV now or never”; it is often “EV later, if the product and price make sense.”

U.S. MINI survey: generational differences in EV demand

BMW’s MINI survey adds a useful generational layer.

- 60% of consumers would consider purchasing an EV.

- 72% of Gen Z consumers would consider purchasing an EV.

- 70% of Millennials would consider purchasing an EV.

- 80% of Gen Z respondents expected charging to take an hour or less.

- 71% of consumers drove less than 75 miles a day.

- 39% cited vehicle cost as a main driver of EV hesitancy.

The age split is especially useful.

Gen Z and Millennials are clearly more open to EV ownership than the broader consumer base, but cost still dominates hesitancy.

That means younger buyers may be ready in mindset before they are ready in budget.

The MINI survey also shows how operating economics can overcome sticker-price resistance:

- 68% of respondents with kids were more likely to buy an EV if operating savings offset pricing concerns.

- 67% of Gen Z drivers said the same.

- 41% of Boomers said the same.

That is a broad appeal pattern, but the intensity differs.

Younger drivers respond strongly, while older drivers are more cautious.

Pull quote: 58% of Americans said their opinion of EVs was unchanged versus the prior year, while 28% said it improved and 14% said it worsened.

BMW driver demographics statistics: model-specific buyer rankings and patterns

When the data shifts from general attitudes to actual BMW model owners, the brand’s premium positioning becomes very concrete.

These buyers are often affluent, male-skewing, and heavily identified with business status or lifestyle utility.

Fast facts:

- 75% of BMW M5s were run as business cars.

- Annual mileage of an M5 often reached or exceeded 100,000 km.

- BMW M5 owners had above-average income.

The M5 stands out as the clearest business-use BMW in the dataset.

High annual mileage and a strong business-car role indicate a vehicle used as a status tool, a travel machine, and a professional asset at the same time.

The BMW 3 Series Coupé tells a different story:

- It is heavily male at 82%.

- It has a high concentration of senior business people at 75%.

- Its owners average ¥74,000 in income.

- Ownership is spread across multiple midlife age brackets rather than a single narrow group.

The Z4, meanwhile, is the most lifestyle-oriented profile in the dataset, with a biggest age group of 30-39 and an average household income of ¥72,000.

That places it firmly in the affluent, image-conscious sports-car segment.

BMW driver demographics statistics and U.S. market scale

Beyond buyer traits, the U.S. sales and manufacturing figures show the scale behind BMW’s reach.

These numbers help explain why BMW can gather such detailed buyer insights in the first place.

| U.S. BMW benchmark | Figure |

|---|---|

| BMW of North America sales in Q1 2026 | 84,231 |

| BMW passenger cars in Q1 2026 | 36,058 |

| BMW light trucks in Q1 2026 | 48,173 |

| MINI sales in Q1 2026 | 6,261 |

| Plant Spartanburg output per day | More than 1,500 vehicles |

| Plant Spartanburg annual capacity | Up to 450,000 vehicles |

| Vehicles assembled at Spartanburg since 1994 | Nearly 7 million |

| U.S. jobs supported | Over 120,000 |

| Annual U.S. economic contribution | More than $43.3 billion |

Why it matters: BMW’s buyer data is backed by serious industrial scale.

That combination of premium brand positioning and large U.S. manufacturing presence is part of what makes the brand’s demographic footprint so influential.

BMW driver demographics statistics: what the numbers say about brand loyalty

One of the strongest loyalty signals in the dataset comes from next-generation vehicle drivers in Japan.

- 87.7% of next-generation vehicle drivers said they want to keep driving next-generation vehicles.

- 58.3% said they want a next-generation or hybrid car in the future.

- 49.6% of gasoline-car drivers said they want to switch to a next-generation or hybrid car.

That suggests a growing but uneven pipeline.

Current adopters are highly loyal, while conventional drivers are still in the evaluation phase.

There is also a perception effect worth noting:

- 75.8% had a favorable impression of next-generation vehicle drivers.

- 36.8% described them as financially comfortable.

- 29.8% described them as smart.

- 27.0% described them as advanced.

Those descriptors matter because they show how alternative-powertrain ownership functions as social signaling.

It is not only about technology or economics; it is also about the image attached to the driver.

Stat spotlight: 62% of Americans consider EV buyers early adopters, reinforcing the idea that EV ownership still carries a pioneer identity.

BMW driver demographics statistics: most important patterns by segment

If you strip the dataset down to its most actionable insights, a few themes dominate.

- Cost sensitivity is universal. Japan shows 88.5% price sensitivity, Canada shows 79% concern over operating costs, and the U.S. shows 40% of future EV buyers citing cost as the main barrier.

- Hybrid-first thinking is strong. In the U.S., 66% would consider a hybrid or plug-in hybrid before a battery-electric vehicle.

- BMW’s premium audience is professional. The 3 Series Coupé and M5 both skew toward business users and higher incomes.

- Gender splits remain pronounced. The 3 Series Coupé is 82% male, the Z4 is more than two-thirds male, and the M5 is also male-leaning.

- Range anxiety appears lower than expected. 75% said 75 miles of daily range is sufficient.

These patterns make BMW’s demographic story unusually coherent: premium, male-skewing in several models, professional in occupation, and increasingly open to electrification when the economics work.

At a glance: BMW’s audience is most likely to respond to a message that combines innovation, practicality, and long-term value — not just premium styling.

BMW driver demographics statistics and the outlook for premium EV adoption

The dataset does not suggest that BMW drivers are uniformly ready to buy an EV tomorrow.

It does suggest something more useful: the audience is curious, practical, and willing to adopt when the numbers make sense.

- Japanese drivers want environmentally friendly cars, but price is the blocker.

- Canadian drivers worry about operating costs and care about environmental impact.

- American drivers value innovation, accept modest daily range, and are open to hybrids or hydrogen alternatives.

- Current BMW ownership skews affluent and professional, which may help premium electrified products find a receptive audience.

That combination creates a clear message map for BMW-like premium brands: lead with innovation, justify the economics, and match the powertrain to the buyer’s usage pattern.